Nigeria's Mobile Gaming Surge and the Myth of the "Next Billion" Player

"The next billion users" is one of those phrases that has been recycled so many times across so many tech sectors that it's stopped meaning much of anything specific. It gets attached to India, to Indonesia, to Brazil, and with increasing frequency over the past few years, to Nigeria — usually accompanied by a population statistic (Africa's most populous country, well over 220 million people) and an implied promise that sheer scale will eventually translate into proportional revenue. Nigeria's mobile download numbers have genuinely earned attention in trade reporting recently, repeatedly showing up among the fastest-growing markets globally. The download number is real. The "next billion" framing built around it deserves more scrutiny than it usually gets.

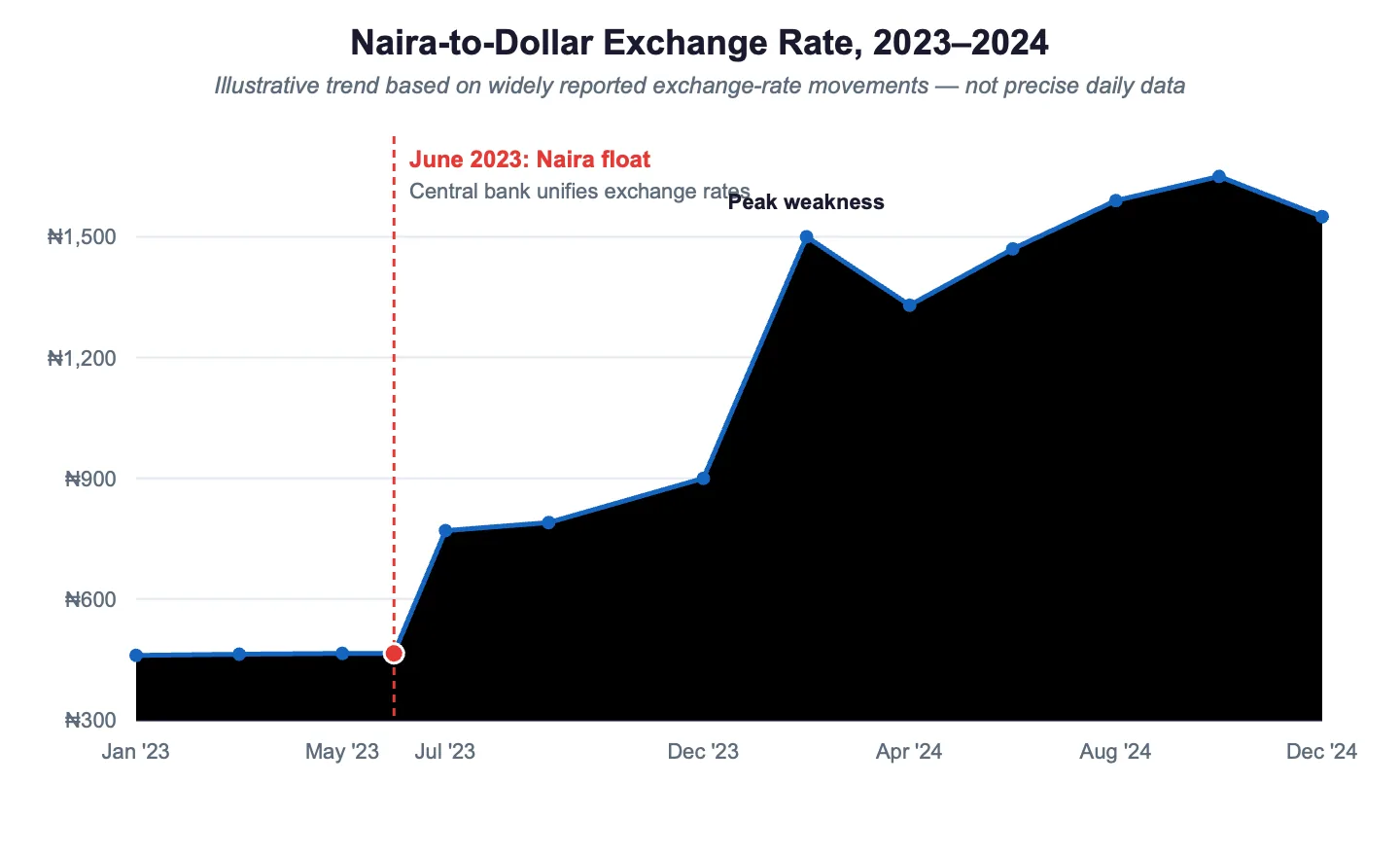

Start with the data cost question, because it's more complicated than the simple "data is affordable" narrative that sometimes gets attached to Nigeria's growth. Nominal data pricing in Nigeria has looked reasonably competitive in regional comparisons for years. But nominal pricing isn't the number that determines whether someone keeps a game open during their commute — what matters is data cost relative to income, and Nigeria's naira has gone through significant, sustained devaluation since 2023, losing a substantial share of its value against the dollar over a relatively short period. That currency move doesn't necessarily change the naira price on a data bundle overnight, but it does mean that any dollar-denominated cost — including in-app purchases priced in USD and converted at checkout — effectively got more expensive for the average Nigerian user, even without a single local price tag changing. That's a very different and much less optimistic story than the one usually implied by population-and-download-growth statistics alone.

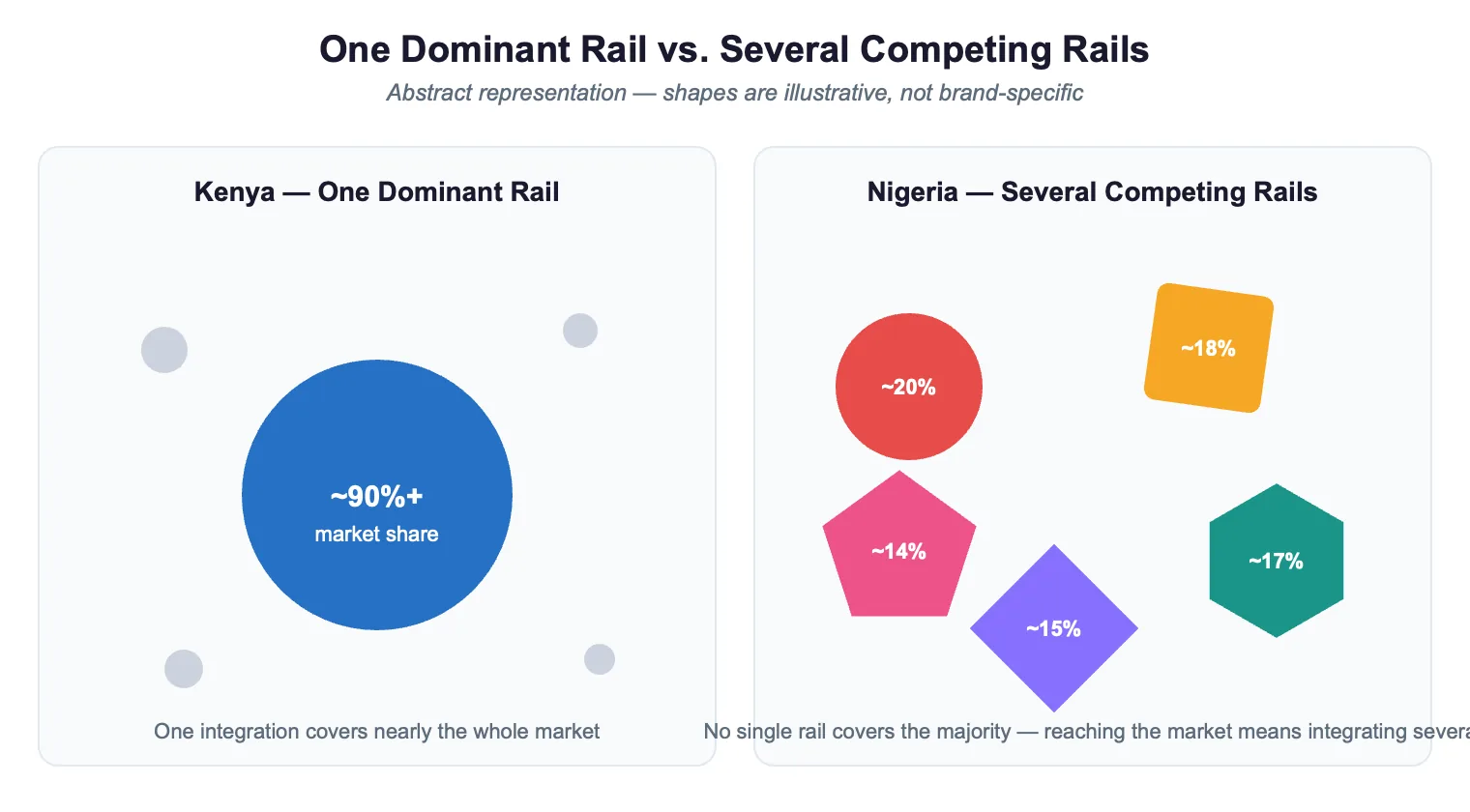

Mobile money infrastructure tells a more genuinely encouraging story, but it's also more complicated than the easy comparison to other African markets. Kenya's M-Pesa is the example most commonly invoked when people talk about African mobile money — one dominant platform, near-universal adoption, a clean story. Nigeria's landscape looks different: a genuinely competitive field of players including OPay, PalmPay, and Moniepoint, alongside traditional bank-linked mobile transfer options, none of which has achieved the singular dominance M-Pesa has in Kenya. That fragmentation has actual product implications for anyone trying to monetize in Nigeria — there's no single payment rail a publisher can integrate and assume covers the bulk of the addressable market the way M-Pesa integration effectively does in Kenya. Reaching Nigerian users on the payment side means accounting for a more genuinely competitive, more fragmented set of options.

There's also a less-discussed infrastructure factor that matters more for sustained gaming engagement than it gets credit for: Nigeria's well-documented power supply instability. Frequent outages affect device charging cycles and can degrade network reliability in ways that aren't really comparable to markets with consistent grid power. A game that depends on long, uninterrupted sessions is fighting against an infrastructure reality that has nothing to do with the game's design and everything to do with whether the player's phone has enough charge and signal to finish a session in the first place.

All three of these factors point toward the same practical conclusion: ad-supported casual games are outperforming premium and IAP-heavy titles in Nigeria by a meaningful margin, and the reasons aren't mysterious once you stop assuming population size alone should predict monetization behavior. A user weighing whether a data session is worth the cost, transacting through a genuinely fragmented mobile money landscape, and dealing with real power and connectivity instability is a user who responds well to rewarded ads — value in exchange for time and attention, no cash or currency-conversion friction required — and responds far less reliably to a premium upfront price or a recurring IAP that assumes stable income and stable infrastructure.

None of this means Nigeria isn't a real opportunity. It clearly is, and the download growth numbers are genuinely earned, not manufactured. It means the opportunity looks different up close than it does from the "next billion" altitude the phrase usually gets used at — less a story about inevitable future revenue scaling with population, and more a story about a market that rewards publishers willing to build specifically around the actual constraints Nigerian users are navigating right now, rather than the constraints a generic emerging-market template assumes they're navigating.

More from the blog

Saudi Arabia's Gaming Investments Are Bigger Than Most People Realize

The easy version of this story writes itself: a petrostate with deep pockets decides gaming looks profitable, buys some equity stakes, collects a press cycle's worth of headlines, moves on. That frami

Ukraine and Romania Are Quietly Becoming Mobile Gaming's Fastest-Growing Markets

Mobile gaming market reports over the past couple of years have repeatedly flagged a cluster of Eastern European and Central Asian markets posting download and engagement growth well above global aver

Why Carrom Never Made It Big Outside South Asia (And What That Says About Cultural Games)

Here's a question that doesn't have a clean answer, and it's worth admitting that upfront rather than pretending otherwise: nobody really knows exactly where carrom came from. The most commonly repeat